REIT Performance

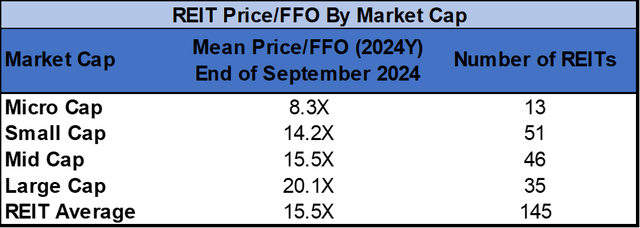

The REIT sector was in the black for the 5th month in a row in September with a +3.09% average total return. REITs outpaced the NASDAQ (+2.8%), S&P 500 (+2.1%) and Dow Jones Industrial Average (+2.0%) in September. The market cap weighted Vanguard Real Estate ETF (VNQ) slightly outperformed the average REIT in September (+3.27% vs. +3.09%) and has significantly outperformed year-to-date (+13.53% vs. +9.61%). The spread between the 2024 FFO multiples of large cap REITs (20.1x) and small cap REITs (14.2x) widened again in September as multiples expanded 0.5 turns for large caps but only 0.3 turns for small caps. Investors currently need to pay an average of 41.5% more for each dollar of FFO from large cap REITs relative to small cap REITs. In this monthly publication, I will provide REIT data on numerous metrics to help readers identify which property types and individual securities currently offer the best opportunities to achieve their investment goals.

Source: Graph by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article

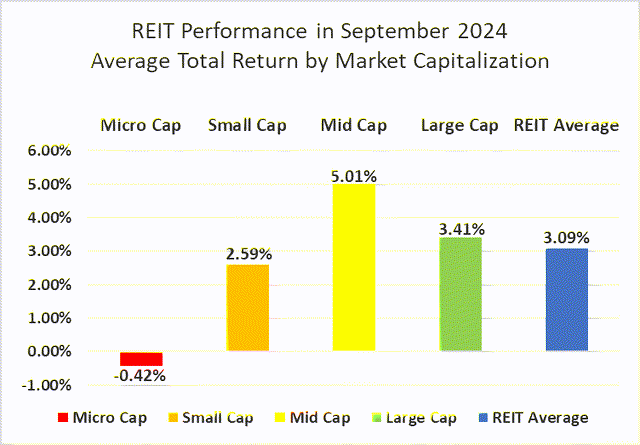

Mid caps (+5.01%) achieved the strongest average total returns in September, followed by smaller gains for large caps (+3.41%) and small caps (+2.59%). Micro cap REITs (-0.42%) continued to underperform their larger peers. Large cap REITs have outperformed small caps by 698 basis points through the first nine months of 2024.

Source: Graph by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article

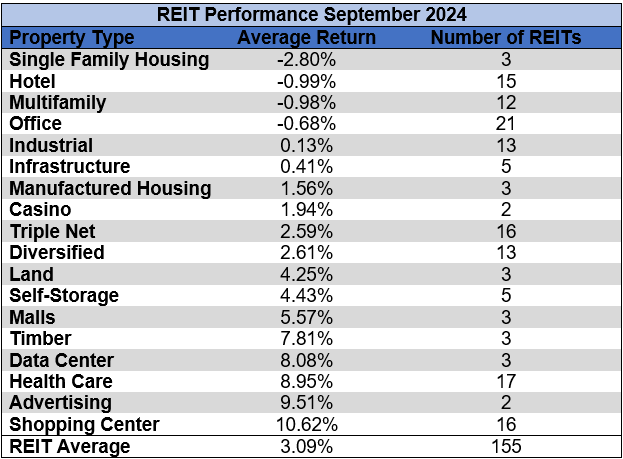

14 out of 18 Property Types Yielded Positive Total Returns in September

77.78% of REIT property types averaged a positive total return in September. There was a 13.41% total return spread between the best and worst performing property types. Shopping Centers (+10.62%) were the top-performing property type in September due to a +130.48% return from the extremely volatile Wheeler REIT (WHLR).

Single Family Housing (-2.80%) underperformed all other property types in September, as all 3 SFH REITs finished September in the red.

Source: Table by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article

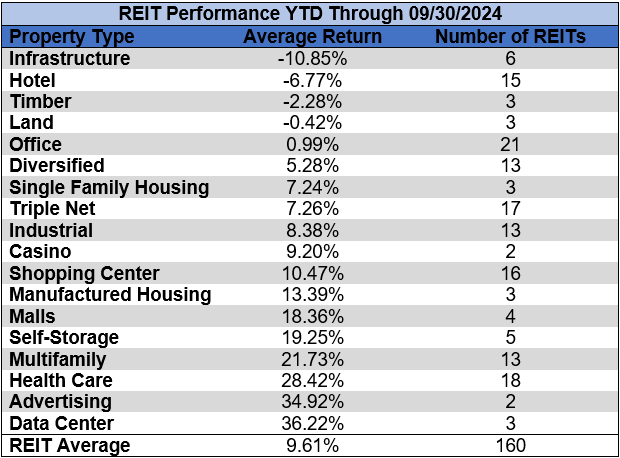

Infrastructure (-10.85%) and Hotels (-6.77%) were the worst performing REIT property types over the first 3 quarters of 2024. Data Centers (+36.22%) and Advertising (+34.92%) have outperformed all other REIT property types thus far this year.

Source: Table by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article

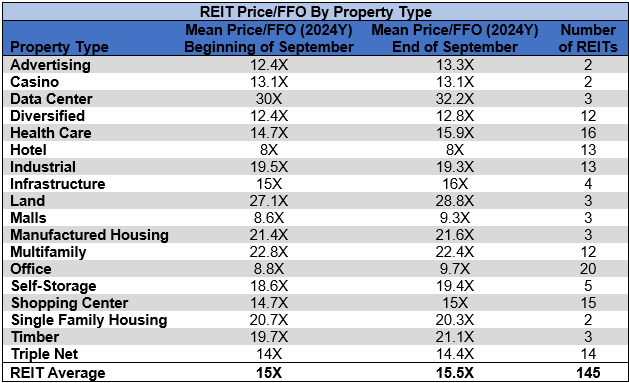

The REIT sector as a whole saw the average P/FFO (2024Y) increase 0.5 turns in September from 15x up to 15.5x. 72.2% of property types averaged multiple expansion, 16.7% saw multiple contraction, and 11.1% had average multiples that remained unchanged during September. Data Centers (32.2x), Land (28.8x), Multifamily (22.4x), Manufactured Housing (21.6x) and Timber (21.1x) currently trade at the highest average multiples among REIT property types. Hotels (8.0x), Malls (9.3x) and Office (9.7x) are the only property types that average single digit FFO multiples.

Source: Table by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article

Performance of Individual Securities

Wheeler REIT (+130.48%) continues to trade in a highly volatile manner, with a +130.48% return in September. The huge spike was fueled by the dismissal of a lawsuit filed against the company by Cedar Realty Trust preferred stockholders (CDR.PR.B) (CDR.PR.C). Despite the share price more than doubling in September, the beleaguered shopping center REIT remains down a whopping -92.63% year to date.

Creative Media & Community Trust (CMCT) (-74.68%) plummeted after the announcement of a redemption of 2.2 million shares of Series A preferred stock and 2.6 million shares of Series A1 preferred stock. The redemption price of these preferred shares will be paid in shares of common stock.

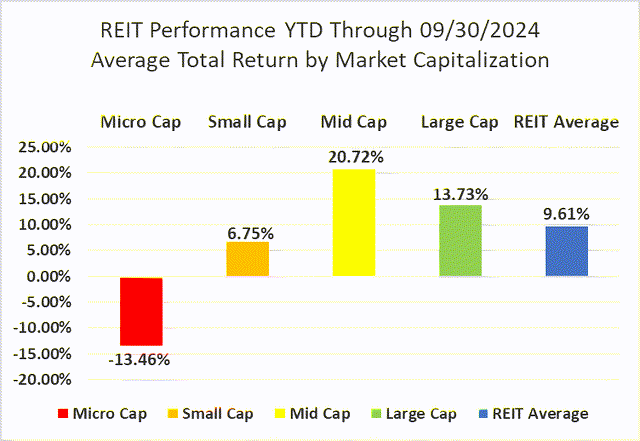

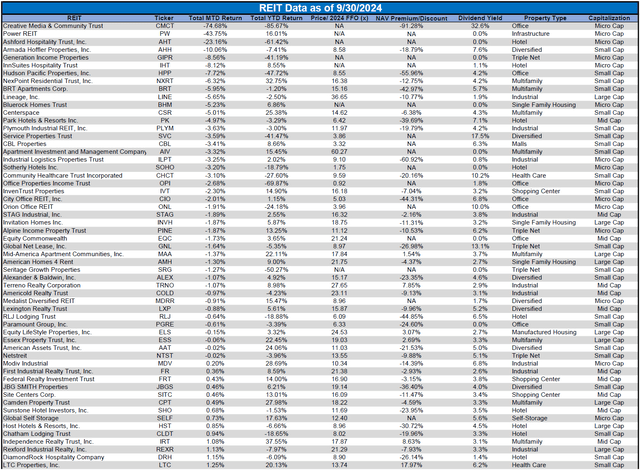

72.26% of REITs had a positive total return in September. During the first three quarters of 2023, the average REIT struggled with a disappointing -6.54% return. The REIT sector has had a much better first three quarters of 2024, however, with a +9.61% average total return.

Source: Table by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article Source: Table by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article Source: Table by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article

For the convenience of reading this table in a larger font, the table above is available as a PDF as well.

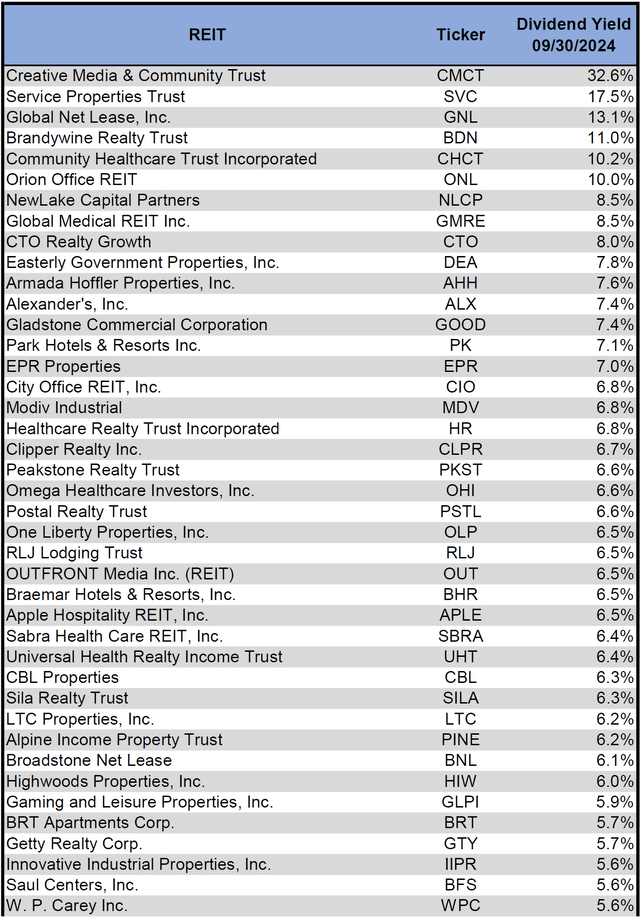

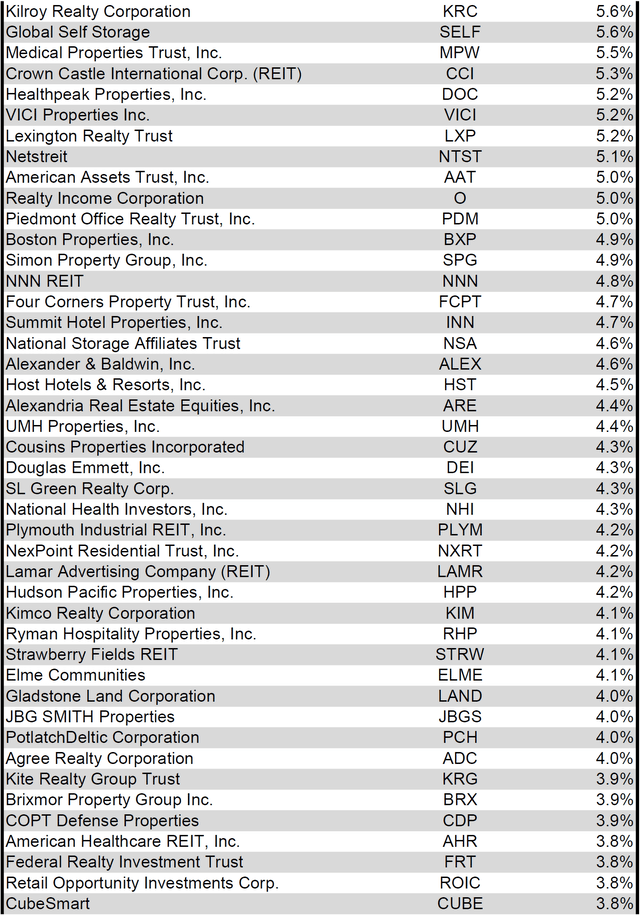

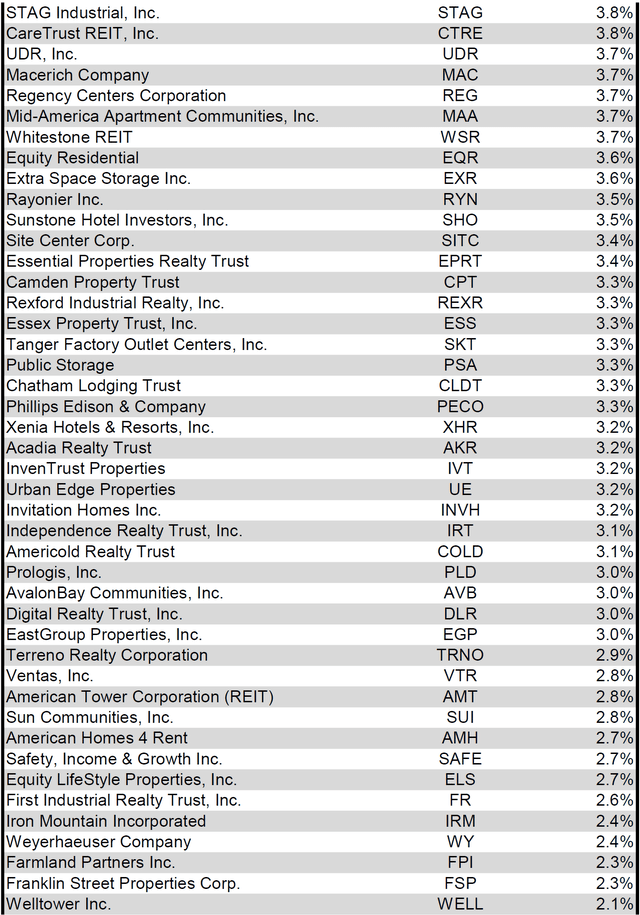

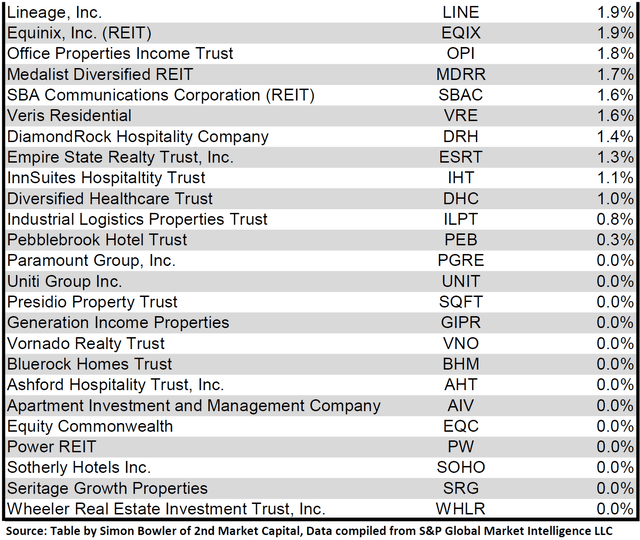

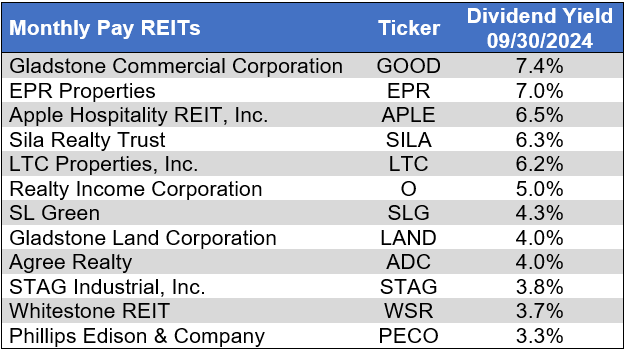

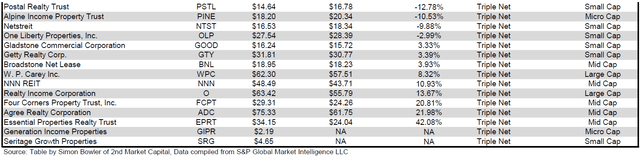

Dividend Yield

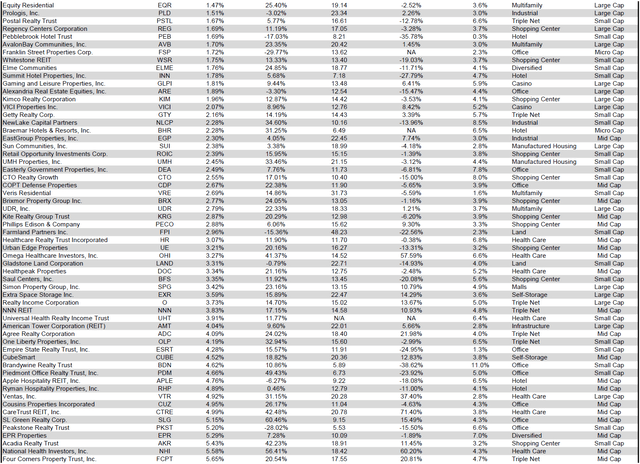

Dividend yield is an important component of a REIT’s total return. The particularly high dividend yields of the REIT sector are, for many investors, the primary reason for investment in this sector. As many REITs are currently trading at share prices well below their NAV, yields are currently quite high for many REITs within the sector. Although a particularly high yield for a REIT may sometimes reflect a disproportionately high risk, there exist opportunities in some cases to capitalize on dividend yields that are sufficiently attractive to justify the underlying risks of the investment. I have included below a table ranking equity REITs from the highest dividend yield (as of 09/30/2024) to the lowest dividend yield.

Source: Table by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article Source: Table by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article Source: Table by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article Source: Table by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article

For the convenience of reading this table in a larger font, the table above is available as a PDF as well.

Although a REIT’s decision regarding whether to pay a quarterly dividend or a monthly dividend does not reflect on the quality of the company’s fundamentals or operations, a monthly dividend allows for a smoother cash flow to the investor. Below is a list of equity REITs that pay monthly dividends, ranked from the highest yield to the lowest yield.

Source: Table by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article

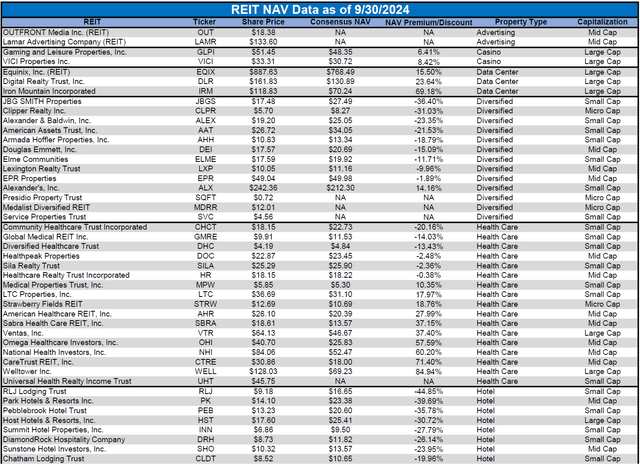

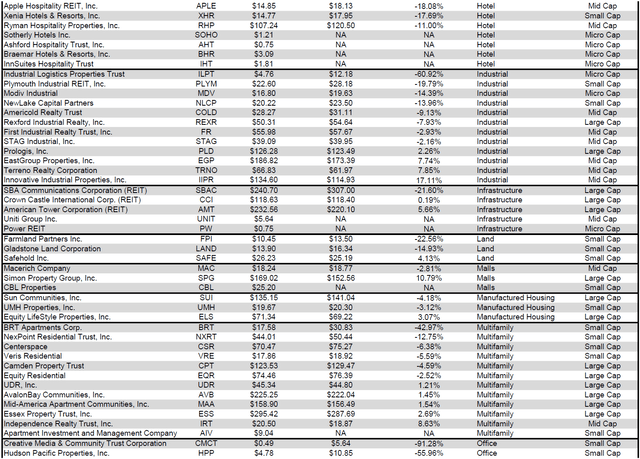

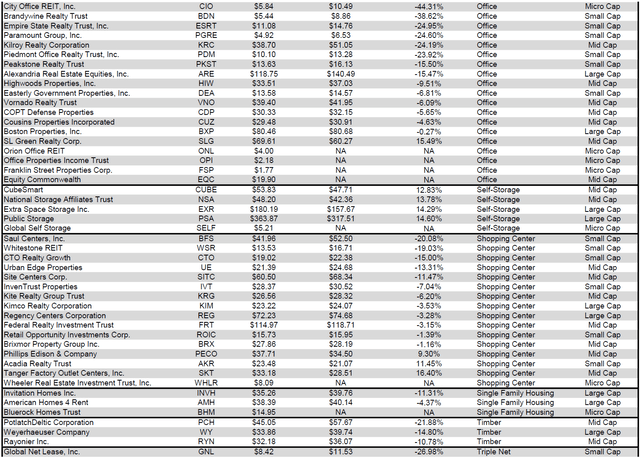

Valuation

REIT Premium/Discount to NAV by Property Type

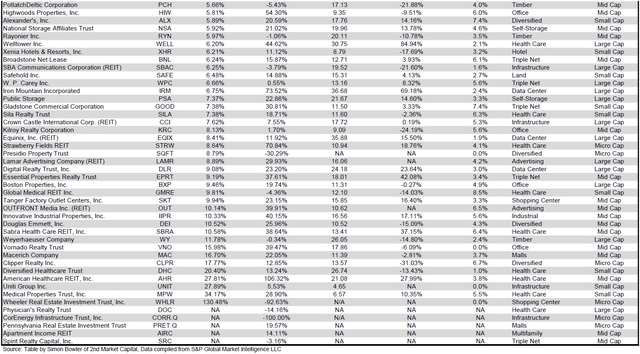

Below is a downloadable data table, which ranks REITs within each property type from the largest discount to the largest premium to NAV. The consensus NAV used for this table is the average of analyst NAV estimates for each REIT. Both the NAV and the share price will change over time, so I will continue to include this table in upcoming issues of The State of REITs with updated consensus NAV estimates for each REIT for which such an estimate is available.

Source: Table by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article Source: Table by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article Source: Table by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article Source: Table by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article

For the convenience of reading this table in a larger font, the table above is available as a PDF as well.

Takeaway

The large cap REIT premium (relative to small cap REITs) widened again in September and investors are now paying on average about 42% more for each dollar of 2024 FFO/share to buy large cap REITs than small cap REITs (20.1x/14.2x – 1 = 41.5%). As can be seen in the table below, there is presently a strong positive correlation between market cap and FFO multiple.

Source: Table by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article

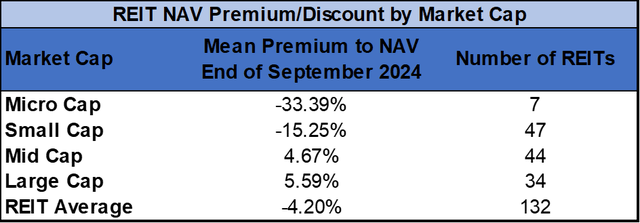

The table below shows the average NAV premium/discount of REITs of each market cap bucket. This data, much like the data for price/FFO, shows a strong, positive correlation between market cap and Price/NAV. The average large cap REIT (+5.59%) and mid-cap REIT (+4.67%) trade at mid-single digit premiums to NAV. Small cap REITs (-15.25%) trade at a double-digit NAV discount, and micro caps (-33.39%) trade at 2/3 of their respective NAVs.

Source: Table by Simon Bowler of 2nd Market Capital, Data compiled from S&P Global Market Intelligence LLC. See important notes and disclosures at the end of this article

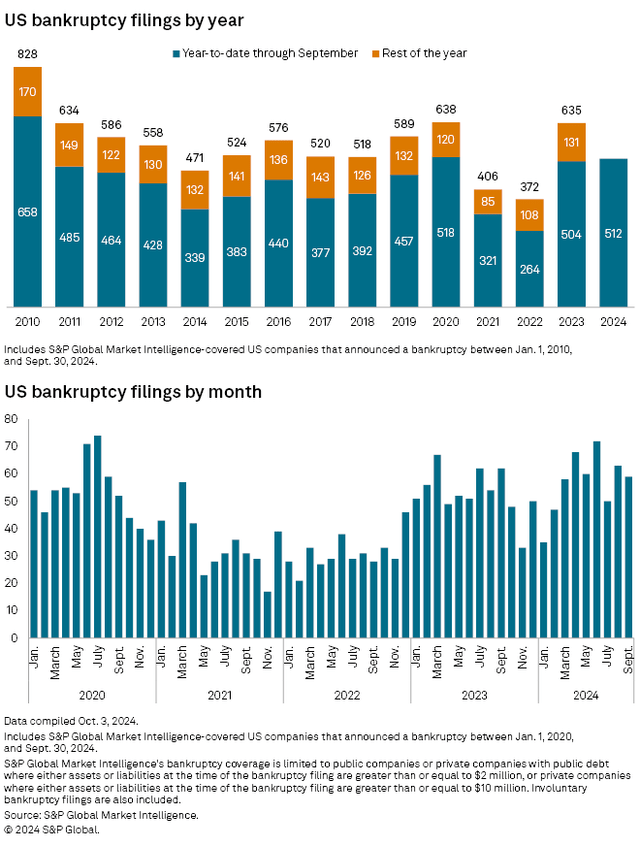

Bankruptcy filings in September declined slightly from August but remained elevated. There were more bankruptcies in the first three quarters of 2024 than during the same period of 2021, 2022 or 2023. There have now been nearly as many bankruptcies YTD as there were during the first three quarters of 2020, a period in which businesses struggled to survive government-imposed lockdowns.

Source: S&P Global Market Intelligence

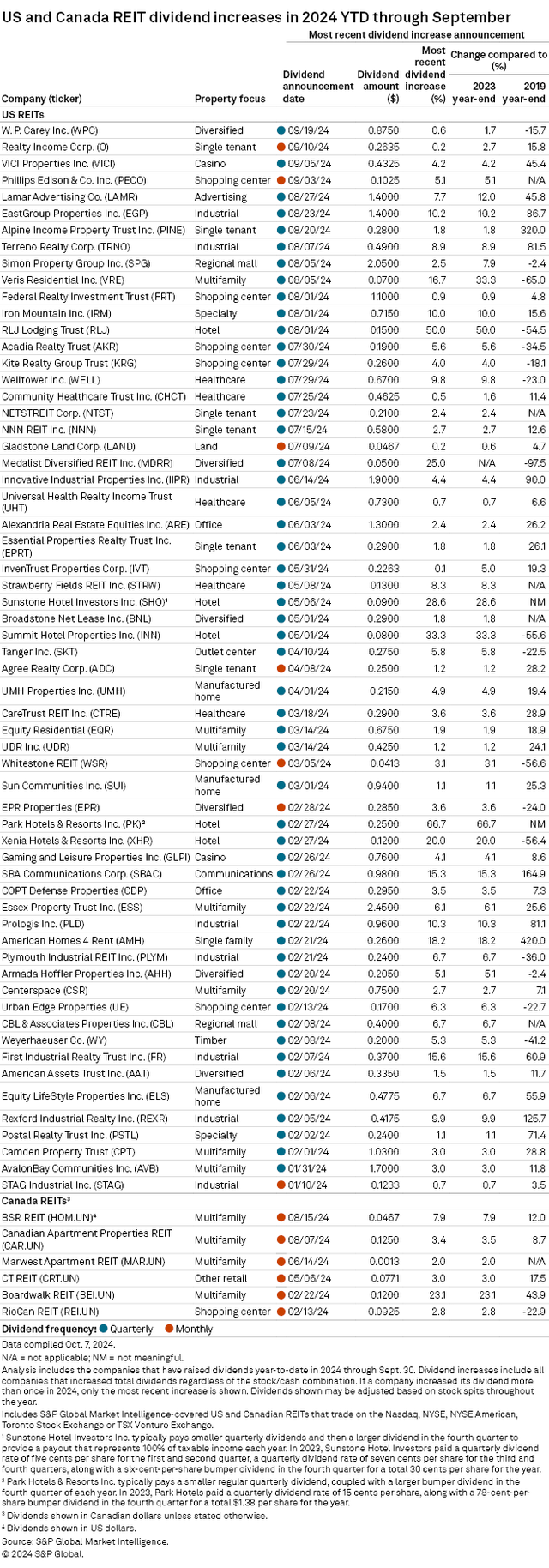

4 REITs announced dividend hikes in September, 2 of which were quarterly and 2 of which were monthly dividends. Phillips Edison & Co (PECO) (+5.1%) and VICI Properties (VICI) (+4.2%) had the largest dividend increases. In total, 61 REITs have announced dividend hikes during the first three quarters of 2024.

Source: S&P Global Market Intelligence

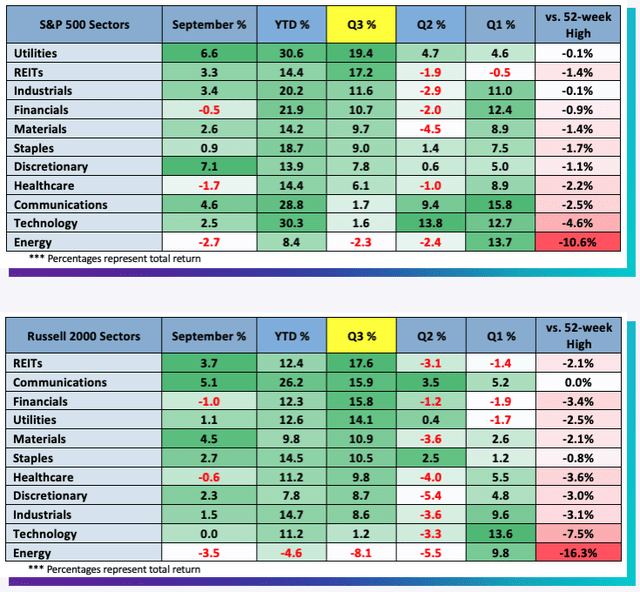

REITs were the 2nd best performing large cap sector in Q3 2024. Additionally, REITs were the small-cap sector with the highest total return in Q3 2024.

Source: NASDAQ

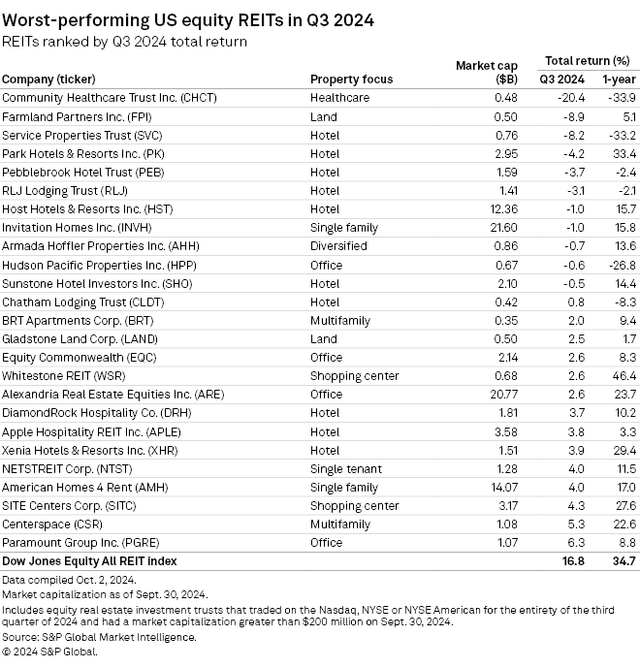

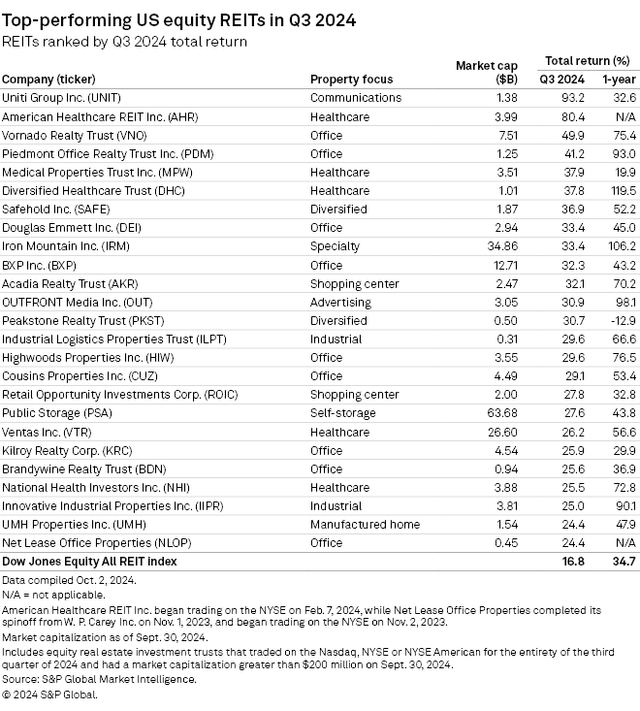

Tremendous Return Variance Across REIT Sector Presents Opportunity for Alpha

Most REITs generated strong returns in Q3, but there were 11 REITs that bucked that trend and finished Q3 in the red. Hotels accounted for more than half of the REITs with a negative total return. Health Care REIT Community Healthcare Trust (CHCT) was the worst underperformer of Q3 with a -20.4% total return.

Source: S&P Global Market Intelligence

Two REITs, Uniti Group (UNIT) (+93.2%) and American Healthcare REIT (AHR) (+80.4%) massively outperformed their peers in Q3. Strong Q3 returns from Diversified Healthcare Trust (DHC) (+37.8%) and Iron Mountain (IRM) (+33.4%) drove them past 100% gains in the past year with +119.5% and 106.2% 1-year total returns respectively.

Source: S&P Global Market Intelligence

The enormous disparity of returns across the sector in Q3 illustrates just how impactful stock selection can be on a portfolio. For example: AHR and CHCT are both Health Care REITs, but AHR outperformed CHCT by over 10,000 basis points in Q3. Huge variance of total return can also be seen within the Office sector, with Vornado Realty Trust (VNO) (+49.9%) outpacing Office peer Hudson Pacific Properties (HPP) (-0.6%) by more than 5,000 basis points. This shows both the opportunity and risk of active management. If insufficient research is done when picking stocks, there are substantial downside risks. However, active management by capable REIT-focused advisors or investors has the potential to yield significant alpha.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here