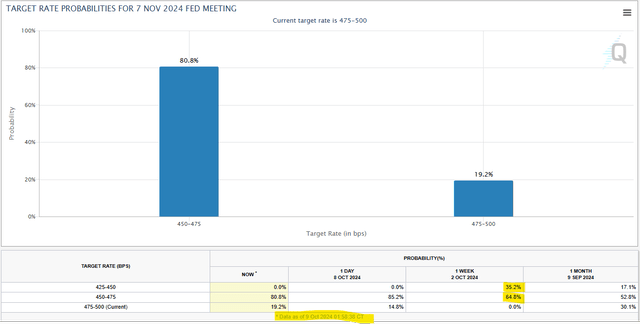

The release of the minutes from the Federal Open Market Committee’s September meeting only intensified the debate on the path and pace of interest rates. This news followed the Bureau of Labor Statistics’ October 4th report of a larger than expected 254,000 jobs increase in September. The effect in the futures market was to evaporate the anticipation that the Fed would repeat with another 50-basis point rate cut at its November 7th meeting.

CME Group

Source: CME Group Fed Watch

Consensus still holds that lower is the direction of interest rates, but that still leaves fixed-income investors guessing as to how far and how fast. Our two-fold objective of securing higher yield for the long term, coupled with some capital appreciation, remains intact. Today we will attempt to forecast how investment in Armour Residential REIT 7.0% Series C Preferred (NYSE:ARR.PR.C), one of our long-time favorites, will play out under current expectations.

The Issue and the Issuer

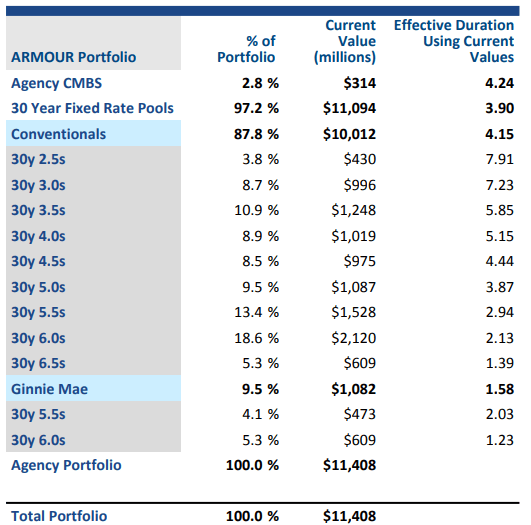

Armour Residential REIT (NYSE:ARR) is an agency mREIT with a current common stock market capitalization of approximately $1B. They lever that equity up approximately 8x to manage a carefully hedged $11.4B portfolio of U.S. Government-sponsored mortgage-backed securities.

ARR 09/30/2024

Source: ARR 9/30/24

That common equity and the income the portfolio generates provide a sufficient capital cushion for us to feel confident in the preferred shares as a hybrid, fixed-income investment, and we’ve been long, to varying degrees, ARR.PR.C for almost five years now.

Portfolio Income Solutions

Source: Portfolio Income Solutions

The $171MM face value of the preferred issuance is senior to the common and carries a fixed 7.0% coupon. The issue is callable after 01/28/2025, but the present interest rate environment and management’s expressed satisfaction with the preferreds fixed coupon structure make us believe the issue won’t be called any time soon. At current market prices, new purchases capture an approximate 7.5% yield, but that dividend is only part of what we are after.

The Short Path to Par Pricing

When the Fed began its inflation-fighting, rate-hiking campaign in March 2022, bond markets headed lower and low-liquidity fixed income instruments, like preferred stocks, became significantly more dislocated. Early on in the rising interest rate environment, we homed in on fixed-to-floating rate preferreds to secure equity and yield protections while the extent of rate increases was yet unknown. Now that the Fed has begun cutting rates, we can more certainly ascertain the ultimate value of fixed coupon issues.

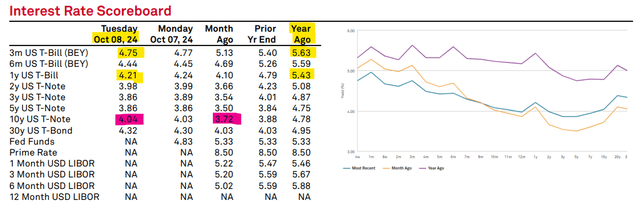

After the Fed cut rates, our initial inclination was to focus on the 10Y T-Note yield to estimate the relative market appeal to high-coupon, discounted preferreds. However, we quickly came to witness the yield curve’s dis-inversion and while shorter term rates were indeed falling, longer duration rates were actually rising.

S&P Capital IQ

Source: S&P Capital IQ

Despite this rate trend, our anticipation that preferred share prices would rise still looked correct. Discounts began to shrink, and many preferred issue prices have risen toward par. Our expectations are being realized; we just misgauged the driving cause.

A Money Market Fund Mountain

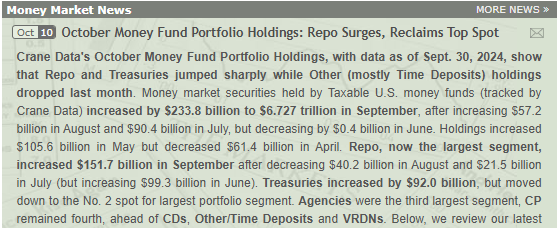

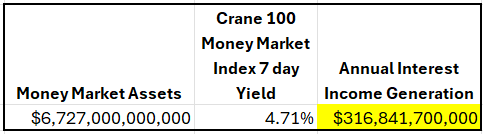

In prior commentary, Dane Bowler observed that money market fund balances had swelled to more than $6T, almost double their historical norm.

Crane Data

Earning a riskless 5%+ return on idle cash obviously has a lot of appeal. Crane Data describes that funds are still flowing into money markets but that may change if yields drop sufficiently.

Crane Data

Even if the Fed slows or stops cutting interest rates, you have to be a little bit in awe of the amount of money fund interest income that needs to be reinvested. REIT preferreds won’t be the likely destination for capital flowing out of money market funds, but $300B dwarfs REIT preferreds trading volume.

2MCAC

Source: 2MCAC

If declining yields cause trillions to flow out of money market funds in pursuit of better returns, it will do so in an environment of yield scarcity. That scarcity will make investors consider riskier options to secure yield, and preferred stocks will become more attractive.

Limited but Attractive Upside

As active fixed income investors, we are drawn to the 7%+ yields available in REIT preferreds today. You can capture a 7.78% yield in purchasing AGNC Investment 7.75% Preferred Series G (AGNCL) at today’s closing price of $24.90. We find discounted issues like ARR.PR.C even more attractive in a declining yield environment because we can secure a high dividend income and potential capital appreciation. If today’s $23.40 share price is pushed to par in a yield scarce environment, that’s a 6.8% gain to add to the 7.47% dividend yield; if rates fall quickly, the combined annualized return could exceed 10%.

Risks of the Future Unknown

Recent economic reporting has dampened expectations for the pace of interest rate declines. If the Fed significantly reduces the speed at which it cuts rates or stops cutting entirely, the sought-after capital appreciation might not materialize. Returns would be capped at dividend yields.

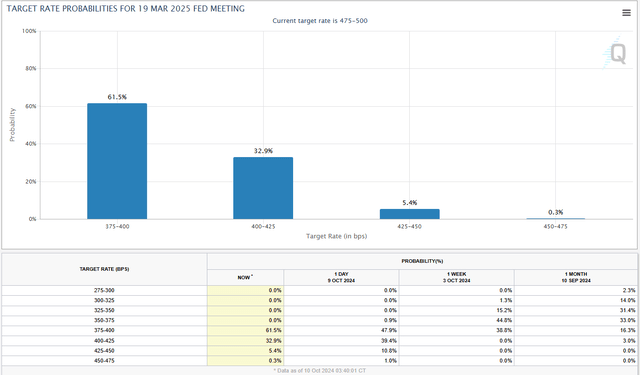

However, while enthusiasm has waned, it has not vanished. Looking out six months, the majority in CME Group’s Fed Watch survey expect the Fed Funds rate to be 100 basis points lower.

CME Group

Source: CME Group

We’ll place our bets and see what happens.

Read the full article here