In our previous article on Liquidia, we discussed the rich catalyst path for value unlocking, we cited significant upside potential to a target of around $16. Today, we are revisiting the opportunity in light of significant legal developments in the last few months.

For starters, in recent weeks the stock price of Liquidia (NASDAQ:LQDA) took a hit as a new discussion around a potential United appeal in front of the Supreme Court emerged. We think this is an overstated risk and that there continue to be no barriers to a full FDA approval at any time, subject to the agency’s efficiency and speed. However, the company is also coming from a legal win at the district court in late May, which we expected and discussed in the previous analysis.

We will provide an overview of the legal situation, but we are not lawyers, so refrain from taking this as legal advice.

The latest United’s desperate effort: SCOTUS

After more than 2 years of intense legal battles, court rulings, PTAB decisions, and Federal Circuit rulings, the story is still not over. United Therapeutics, driven by its ultimate goal of preserving a monopolistic position in a multi-billion drug market, recently filed a new action before the United States Supreme Court.

This is a copy of the petition that was filed by United on June 10, 2024. This is essentially an appeal of the Federal Circuit decision issued in December, which ruled that the PTAB decision on patent ‘793 was valid. This means that the patent is still unpatentable, and thus Liquidia is not infringing it.

After this ruling, a years-long injunction prohibiting the FDA from issuing a full approval was removed in March, allowing for the commercialization of YUTREPIA at any time. So how exactly will this action change things? The answer is, that it most likely won’t. Out of more than 7,500 cases presented in front of SCOTUS, only around 100 will actually receive an opinion from the court, while the others won’t even appear in front of the judges, according to this Valorem Research article.

However, on July 11, the news that the court demanded an answer to the Petition from Liquidia sent the stock in a negative spiral for a few days, dropping as much as 15% in a day. But what is United arguing precisely? According to this legal analysis:

UTC contends that the PTAB violated § 312 by relying on grounds and printed publications not raised in Liquidia’s initial IPR petition. The Federal Circuit affirmed the PTAB’s decision, holding that it would defer to the PTAB’s discretion as long as the new arguments were “not inconsistent with” the initial petition.

Basically, the arguments make some reference to the recently overturned Chevron Deference. The case is centered around the PTAB’s discretion in evaluating new evidence and when this evidence should be properly presented. While we are not in a position to discuss the technicalities, we are positive for the following reasons:

-

Historical data on case acceptances and opinions issued implies a 2-3% success rate for United, and thus a 97-98% success rate for Liquidia

-

We think the merits are weak given (1) an undisputed ruling at the Federal Circuit where no judge was against the decision, and (2) a well-established practice of presenting additional evidence in responses during PTAB proceedings

-

There continues to be no injunction and the FDA can approve the drug even during SCOTUS proceedings, if any, and also later until adversary proceedings at the Federal Circuit determine against

Essentially, time is on Liquidia’s side this “time”. We feel confident the FDA will soon approve YUTREPIA after more than 6 months of delay since the PDFUA date on January 25, 2024.

The District Court Ruling on Parent ‘327 Strengthen Liquidia’s Position Once Again

Just as a summary of the ongoing actions that the company is facing, we provide a transcript from the April 1 press release issued by the company.

In the first action, UTHR filed a lawsuit against FDA in the U.S. District Court for the District of Columbia (Case No. 24-484), and a motion for a temporary restraining order and preliminary injunction, seeking to prevent FDA from approving Liquidia’s amended NDA. After a hearing on March 29, Judge Bates, who is presiding over this lawsuit, denied UTHR’s motion. Specifically, the Court held that the subject of UTHR’s case, FDA’s acceptance of Liquidia’s amended NDA for substantive review, is not a final agency action that UTHR can challenge in court.

This was the first win against another desperate United action against the FDA to delay the approval.

In the second action, UTHR filed a lawsuit against the Company in Delaware District Court (Case No. 23-975) alleging that YUTREPIA would infringe U.S. Patent No. 11,826,327 (‘327 patent), which issued in November 2023. UTHR has filed a motion for preliminary injunction to block Liquidia from launching YUTREPIA for PH-ILD. Briefing on UTHR’s motion remains in process.

This was the key action that Liquidia then filed at the District Court on the newly issued patent 327. We reported in our article in mid-May that this was a relevant catalyst that could unlock value. Right after our analysis, a ruling came in this case that caused a 20%+ increase in LQDA share price:

“Although Plaintiff has shown a likelihood of success as to infringement of claims 1, 6, 9, and 10 of the ‘327 patent,” Plaintiff has failed to show the Defendants’ obviousness challenge lacks substantial merit,”

In particular, the request by UTC for a new preliminary injunction was denied, keeping the path clear for a potential imminent approval.

Valuation Framework Remains Favorable With Deep Discount to Potential Market Cap

The original analysis we posted remains valid, and we firmly believe that Tyvaso’s sales figures support a generous EV for Liquidia as well. While UTC has not reported Q2 numbers yet, we think the market may even positively react to those figures by reflecting a share price increase in LQDA.

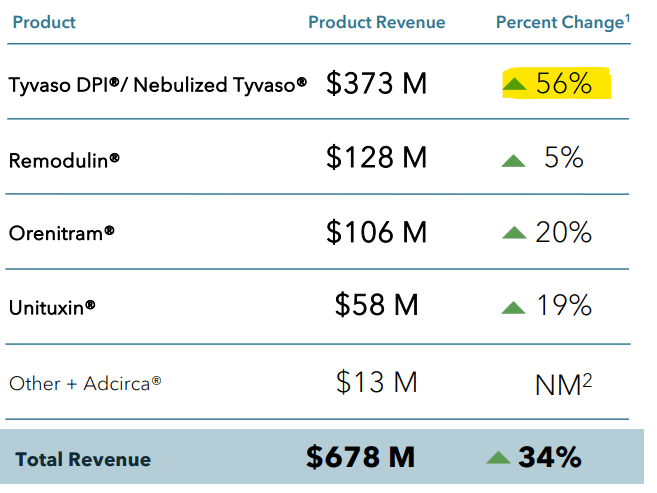

UTHR Sales by Product – Q1 (Q1 Presentation)

By looking at UTC’s figures, it is easier to understand why their legal strategies are so aggressive against the company. Tyvaso and its nebulized version are the fastest-growing products in their portfolio. The revenue contribution is also the largest, making a potential FDA approval of the extended LQDA label (i.e. including PH-ILD), a dangerous development for their valuation.

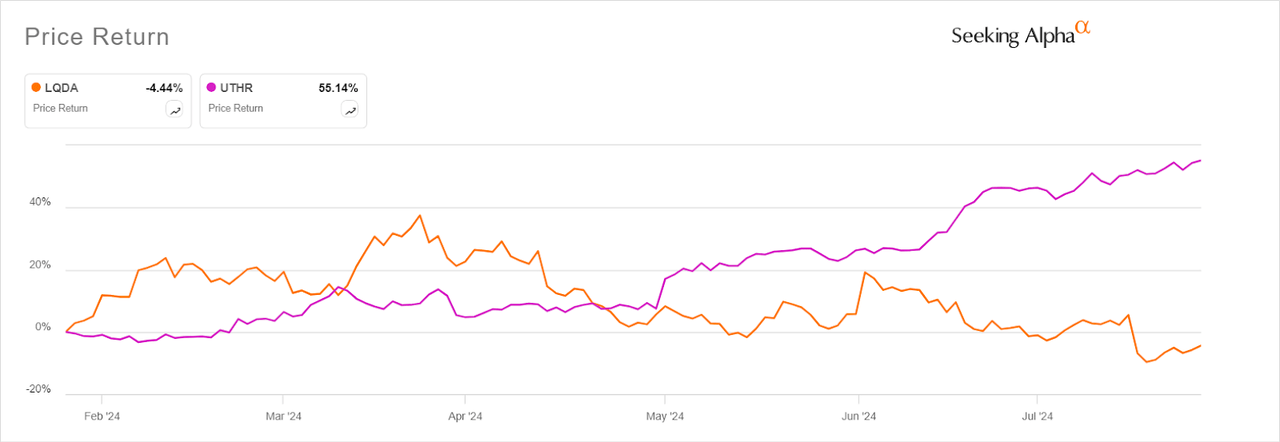

Price Spread UTHR vs LQDA (Seeking Alpha)

However, the market seems not concerned with these developments, and the spread between LQDA and UTHR share prices increased in UTHR’s favor. If this continues, we may consider a spread trade instead of a purely directional position on Liquidia.

Risks: Legal and Time-related

We believe that the recent financing deal announced in January, when the company received around $100 million in funding from HCRx and other Patient Square Capital, signals that the legal risk has already been minimized. However, we cannot rule out a negative impact from a SCOTUS action, or a loss at the District Court trial on patent 327 in 2025.

This needs to be added on top of the timing issues with the much-awaited FDA approval. After more than 6 months, the agency has not come back yet with a decision, and this may weigh on the discounted value of YUTREPIA exclusive sales before their own patent expiration.

All in all, we are confident that the potential reward far outpaces the risks embedded in this investment, but we are also carefully monitoring the situation.

Conclusion

We think Liquidia again offers a very interesting entry point after a legal development caused an undeserved share price drop. The outlook on their legal position ahead of a potential imminent FDA approval is still very strong, and the upside is intact. United Therapeutic’s results on Tyvaso sales also continue to present a compelling point in favor of Liquidia. We reiterate our buy rating.

Read the full article here